As taxpayers, we like to think that every dollar is put to good use. It's very frustrating to see our taxes wasted. But, every year, vast swaths of public money are frittered away on a service that adds very little value to anyone except those who are paid to deliver it. I'm talking about active money management

Public employee retirement funds are designed to provide retirement income to state and local government employees, including teachers, police officers, firefighters, and other public sector workers. These funds are typically defined-benefit plans, meaning they promise a specific monthly benefit at retirement, which is calculated based on factors such as salary history and years of service.

These pensions are funded through a combination of employee contributions, employer contributions, and investment returns. Employees generally contribute a fixed percentage of their salary.

The sums of money involved are eye-wateringly huge. As of recent estimates, U.S. public pension funds collectively manage around $4.5 trillion in assets, and they pay out hundreds of billions of dollars to retirees every year.

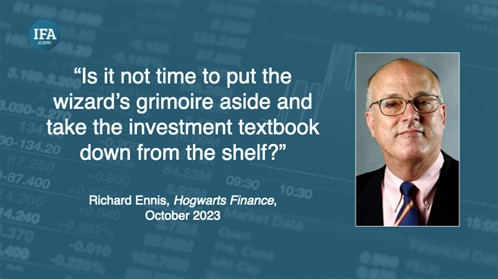

It's in the interests of both taxpayers and plan members that these pension assets are managed as efficiently as possible. Sadly, though, that is all too often not the case. According to an October 2023 paper by investment consultant Richard Ennis called Hogwarts Finance, since the global financial crisis of 2008-09, public pensions have achieved lower returns than simple low-cost index funds.

This underperformance has averaged between one and two per cent a year. That may seem like a modest amount, but compounded over time, it can make a massive difference.

Lack of Intellectual Rigor

The problem, writes Ennis, is a lack of intellectual rigor in institutional fund management. "The professionals," he writes, "are ignoring their canon. Lawyers coming before the bar are expected to know the law. Physicians, conspicuously, in my experience, attempt to adhere to the best medical science. Engineers do not improvise when designing bridges. But the people managing institutional assets behave like they attended Hogwarts School of Witchcraft and Wizardry."

Ennis's paper highlights several mistakes commonly made by the Chief Investment Officers and consultants who manage public pension assets. For example, they overestimate the diversification benefits of alternative investments like private equity, real estate, and hedge funds, and yet underestimate the cost of using them. Ennis also shows how they give the impression that their returns are higher than they are by measuring their performance against the wrong benchmarks.

It all adds up to a colossal waste of money. Ennis estimates that "the resulting economic inefficiency costs beneficiaries in the US at least $100 billion a year."

Quotes and pictures are utilized for illustrative purposes only and should not be construed as an endorsement, recommendation, or guarantee of any particular financial product, service, or advisor.

Quotes and pictures are utilized for illustrative purposes only and should not be construed as an endorsement, recommendation, or guarantee of any particular financial product, service, or advisor.A Worldwide Problem

It's not just in the U.S. that money is being wasted on public pensions. It's a problem all over the world.

Recently, for example, Andrew Coyne, a financial correspondent for the Globe & Mail in Toronto, highlighted similar problems with the Canada Pension Plan Fund. The CPP Fund is a contributory, earnings-related social insurance program, designed to give ordinary Canadians financial security in retirement.

The CPP's investment board, Andrew writes, has "essentially turned itself into a giant hedge fund, picking stocks, taking seats on boards, and plunging heavily into an increasingly esoteric mix of assets: real estate, private equity, infrastructure, and God knows what else.

"The fund's staffing levels, consequently, exploded, from roughly 150 employees in 2006 to more than 2,100 today. So did its costs, particularly the fees paid to external investment managers: from $36 million in 2006 to $3.5 billion in 2024, a near hundredfold increase.

"Over all, combining management fees, operating expenses and transaction costs, the fund's expenses now exceed $5.5 billion annually. All that has been achieved in the course of that 18-year, $46 billion spending orgy has been to lose $42.7 billion for the nation's pensioners."

Public Pensions Should Use Index Funds

For 25 years, IFA.com has consistently cautioned against using complex, active investment strategies. The evidence is overwhelming that investors are better off with a diversified portfolio of low-cost index funds instead. And what's best for ordinary investors is also best for public pensions.

Take, for instance, Nevada's Public Employees' Retirement System, one of the country's best-performing state pensions. Until recently, it has been managed by just one-person, Chief Investment Officer Steve Edmundson.

Instead of paying consultants and active managers to try to beat the market, Edmundson keeps things simple, focusing on efficiency and cost control. Apart from modest holdings in property and private equity, the vast bulk of the assets he manages is invested in passive equity and bond funds. When asked by the Wall Street Journal to describe his daily trading strategy, Edmundson replied: "Do as little as possible, usually nothing."

Quotes and pictures are utilized for illustrative purposes only and should not be construed as an endorsement, recommendation, or guarantee of any particular financial product, service, or advisor.

Quotes and pictures are utilized for illustrative purposes only and should not be construed as an endorsement, recommendation, or guarantee of any particular financial product, service, or advisor.Investment Consultants are Conflicted

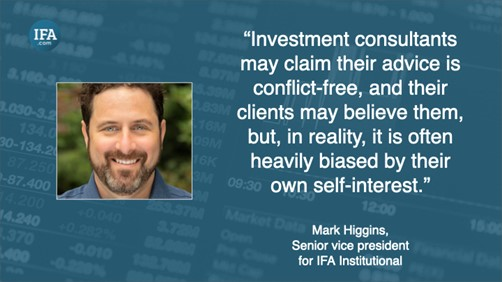

All of this begs an obvious question: if low-cost index funds really are the best solution for public pensions, why don't more pensions take the same approach as Nevada does? As IFA's Mark Higgins recently explained in an article for the CFA Institute, the main problem is an unspoken conflict of interest at the heart of investment consulting.

"Investment consultants may claim their advice is conflict-free, and their clients may believe them," Mark writes, "but, in reality, it is often heavily biased by the investment consultants' own self-interest." Why? Because, for consultants, index investing poses an existential threat. "If most clients are better off simplifying their portfolios," Mark goes on, "replacing active managers with low-cost index funds, and avoiding alternative asset classes, then the current investment consulting business model is obsolete."

For us, this sorry state of affairs is unacceptable and completely unsustainable. As a firm, IFA is committed to raising awareness of the failings in the U.S. public pensions system and to doing something about them.

If you're a pension fund trustee and you would like to find out more about index investing and how it can deliver better outcomes, and more cost-effectively, why not get in touch? We would love to talk to you.

Pension plan members and taxpayers alike deserve better. It's time to put a stop to this scandalous waste of resources.

Robin Powell is the Creative Director at Index Fund Advisors (IFA). He is also a financial journalist and the editor of The Evidence-Based Investor. This article reflects IFA's investment philosophy and is intended for informational purposes only.

This article is intended for informational purposes only and reflects the perspective of Index Fund Advisors (IFA), with which the author is affiliated. It should not be interpreted as an offer, solicitation, recommendation, or endorsement of any specific security, product, or service. Readers are encouraged to consult with a qualified Investment Advisor for personalized guidance. Please note that there are no guarantees that any investment strategies will be successful, and all investing involves risks, including the potential loss of principal. Quotes and images included are for illustrative purposes only and should not be considered as endorsements, recommendations, or guarantees of any particular financial product, service, or advisor. IFA does not endorse or guarantee the accuracy of third-party content. For additional information about Index Fund Advisors, Inc., please review our brochure at https://www.adviserinfo.sec.gov/ or visit our website at www.ifa.com.

X

X