In the past, we've written extensively about the value premium as a key driver of expected returns. Along these lines, we thought it might be worthwhile to explore the academic genesis of another factor tied to market risk — the discovery of the small-cap premium.

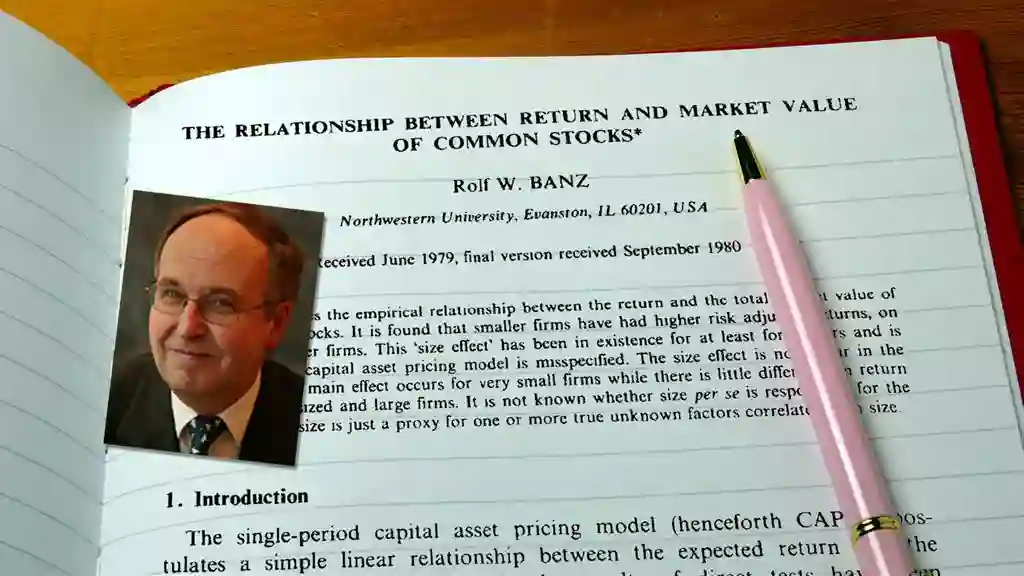

Many investors probably assume that Nobel laureate Eugene Fama and his frequent research partner, Kenneth French, were the ones who uncovered the small-cap premium. Although both were important in advancing such work, Rolf Banz — a professor at Northwestern University at the time and a former grad student of Fama's at the University of Chicago — is credited with authoring the first research piece that formally identified such a factor of stock investing.

His landmark paper, "The Relationship Between Return and Market Value of Common Stocks," was published by the Journal of Economics in 1981. Utilizing stock data from the Center for Research in Security Prices (CRSP), which at that time only had NYSE listings, Banz studied a fairly extensive period that stretched from 1936 through 1975. He concluded:

"It is found that smaller firms have had higher risk adjusted returns, on average, than larger firms. This ‘size effect' has been in existence for at least forty years and is evidence that the capital asset pricing model is misspecified."1

Banz's paper was historically significant in practical finance, as 1981 marked the founding of Dimensional Fund Advisors (DFA) by David Booth and Rex Sinquefield. (As a pioneer in factor-based investing, Dimensional is our Investment Committee's favored fund family in designing and implementing IFA Index Portfolios.)

Also worth noting, the fund provider's initial offering was the DFA U.S. Micro Cap Portfolio. It was created to capture the size premium by staying in the lowest two size deciles. At the same time, it's managed — just like other DFA funds — using a mandate of trading in a rather patient and opportunistic value-styled manner. The fund is rated by Morningstar as one of the broadest and most diversified in its category.

As the table below shows, DFA's U.S. Micro Cap Portfolio has provided investors with accurate and comprehensive exposure to micro-cap stocks over the long haul.

Still, there's a lingering question that Banz raised in his landmark paper. At the end of the piece's abstract, he wrote:

"It is not known whether size per se is responsible for the effect or whether size is just a proxy for one or more true unknown factors correlated with size."

Either way, we've applied the work of Banz to effectively serve as a bridge to later research identifying other factors used in calculating a diversified stock portfolio's expected return. As a result, a traditional IFA Index Portfolio is tilted towards the compensated equity risk-and-return factors of small-cap and value. Our investment selection process also includes funds that screen stocks by corporate profitability and how much investment capital a company makes in order to grow assets.

As applied by DFA's family of mutual funds and exchange-traded funds, these dimensions of stock returns have proved in our own research — as well as the experience we've gained by managing globally diversified fund portfolios for more than two decades — to work in complementary fashion.

The chart below shows how powerful of an explanatory force size, value and profitability are as standalone factors. Taking advantage of funds that combine all three in an integrated fashion, however, tilts the odds of outperformance even more for our investors.

Of course, Banz's work can't be viewed in a vaccum.

Indeed, the young academic credited much of his seminal research to earlier work done for his dissertation paper at the University of Chicago. In introducing "The Relationship Between Return and Market Value of Common Stocks," Banz thanked "for their advice and comments" Fama and other members on his dissertation committee at the school, which included financial luminaries Myron Scholes, Roger Ibbotson and Merton Miller.

In this regard, it's worth noting that Banz's research garnered enough attention in the financial sciences to be utilized by Fama himself. This is significant to point out since he and French, who at the time also taught at the University of Chicago, published a series of research papers in the early '90s establishing the so-called Fama/French Three-Factor Model.

Sythesizing earlier theories about how expected returns should be determined, Fama and French expanded on the Capital Asset Pricing Model (CAPM). In such a statistical framework, market risk — measured by the excess return of a broad equity market portfolio relative to a risk-free rate — was the primary method to calculate expected returns.

While including market risk, Fama and French found expected returns to also be significantly tied to a diversified stock portfolio's sensitivity (i.e., exposure) to two other common risk factors. One related to value, which was calculated by comparing returns of a portfolio of high book-to-market (value) stocks to a portfolio of low book-to-market (growth) stocks. The ratio (BtM) is influenced by a company's growth prospects, shareholder risk and cash-flow generation.

The three-factor model indicated that value beat growth stocks over longer periods. It also built on Banz's earlier identification of market capitalization size as an important factor in determining a diversified equity portfolio's expected return. Fama and French are credited with advancing the work of Banz with a more comprehensive and integrated model for calculating expected returns.

Fama was also instrumental in devising a technical foundation for Banz's early research into systematic investment methodologies. How so? Banz relied heavily on a mathematical technique known as regression analysis. Not so coincidentally, this type of number crunching was initially brought to the forefront of financial sciences by research conducted by Fama and James Macbeth in 1973.2

Running mutliple regressions, Banz was able to separate different types of data from all types of markets and time periods. This related to what he described as long-term patterns of risk as well as returns. In turn, such a refined measurement of markets established what he termed as the size effect.

This raises another interesting back story to our review of the contribution Banz has made to the study of asset prices and factor investing.

The environment that market researchers worked in during the late '70s and early '80s was much different than today's highly automated world. In fact, "The Relationship Between Return and Market Value of Common Stocks" took more than five years to be processed, reviewed and published.

After spending an extended timeframe compiling and analyzing the data, Banz actually submitted his finished research paper for peer review in 1979. But it took him until 1981 to get a green light for final publication in the Journal of Financial Economics. Considering how much bigger of a footprint his work provided for those trying to more precisely figure estimated returns, some investors might be rather incredulous that these findings weren't brought to press sooner.

But again, this is an important footnote to the size factor's story. It stands as a reminder of how far scientific methodologies as applied to portfolio management have progressed over the years. To be fair, though, this is far from suggesting that getting substantive market research published in respected financial journals these days is anything less than a rigorous — and often relatively lengthy — undertaking.

Our aim with this article, though, is to highlight an important piece of history in the evolving study of systematic investing. We hope that more investors will appreciate how arduous of a task market researchers face in digging deeper into what drives long-term returns, especially in those pre-personal computing days. At IFA, our investment committee salutes the ingenuity and persistence that Banz exhibited in pioneering the existence of the size premium.

Footnotes:

1Banz, Rolf W. 1981. "The Relationship Between Return and Market Value of Common Stocks." Journal of Financial Economics, vol. 9, no. 1(March):3-18.

2Fama, Eugene F., and James D. Macbeth. 1973. "Risk, Return, and Equilibrium: Empirical Tests." Journal of Political Economy, vol. 81, no. 3 (May-June):607-636.

This is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, product or service. There is no guarantee investment strategies will be successful. Investing involves risks, including possible loss of principal. IFA Index Portfolios are recommended based on time horizon and risk tolerance. Take the IFA Risk Capacity Survey (www.ifa.com/survey) to determine which portfolio captures the right mix of stock and bond funds best suited to you. For more information about Index Fund Advisors, Inc, please review our brochure at https://www.adviserinfo.sec.gov/

X

X